As we head into the fourth quarter of 2018, investors have plenty to worry about.

From the yield curve pointing to rising odds of a US recession, to an increase in external factors that are driving up both international and domestic market risk, you might be mulling over ways to reduce exposure. While current market conditions offer a compelling reason to be more risk-averse, how do you sell this to your clients especially if the economy keeps chugging along, at least for a while?

Taking broad stock market risk offers an important source of return for many portfolios, but it isn’t the only one. By taking a multifactor approach, investors can seek additional sources of return and diversify their strategies. This is a way broad macro shocks can hold less sway over performance. This approach comes in especially handy when behavioral biases hijack portfolio design.

A traditional portfolio invests in indexes and diversifies across asset classes to gain the risk-lowering benefits of diversification. Indexing allows investors to diversify away company-specific risk (“Don’t hold only WorldCom/Enron stock, and you’ll buffer against those types of calamities,” or, “Don’t keep all your eggs in one basket”). But indexing doesn’t remove systematic risk (“You own the S&P 500 in 2008,” or, “The great egg-basket fire of 2008 has destroyed 2/3rd of your eggs”). This systematic risk is a factor that accounts for stock indexing’s positive expected returns. If you index, with few exceptions, portfolio shocks from bad economic news are part of the deal.

That’s not the only difficulty: investors are human. They want greater returns, especially when stocks are doing well. They forget about risk. They end up abandoning conservative strategies, overinvesting in risky assets when the market seems friendly. This sets up for a painful scenario. Riskier assets tend to become more correlated in rocky markets. Suddenly, a seemingly diverse portfolio doesn’t seem so prudent.

Fortunately, there is another approach. There are other risk exposures – factors – with uncorrelated exposure to macroeconomic shocks. Taking different types of risk besides broad market risk is a key component of a multifactor approach, and this strategy diversification helps shield investors from seemingly unavoidable downturns.

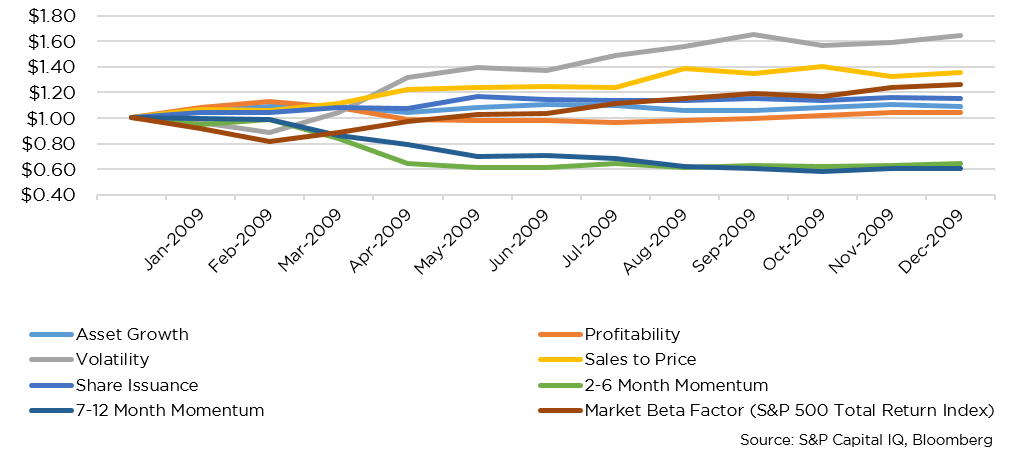

The below chart shows performance of seven different hypothetical long-short portfolios[i] designed to expose investors to different factors besides macroeconomic risk. These portfolios represent pure factor exposures. They have positive expected returns because they capitalize on flaws in human psychology that cause relative (“cross-sectional”) mispricing within the market. For example, the asset growth anomaly is based on the observation that investors tend to overvalue companies with growing assets, and undervalue companies with shrinking assets.

Crisis Recovery: 2009 Value of $1 Invested in Individual Factors

It should be clear from the chart, which tracks performance of these factors since the start of the recovery from the Great Financial Crisis, that these different factors have experienced a broad variety of returns. Importantly, these factors also exhibit low or zero correlation to each other. And just as investors can invest in multiple companies at once, they can also invest in multiple factor exposures at once. They can thus capture positive expected returns while reducing correlations, and potentially their exposure to broad macroeconomic shocks.

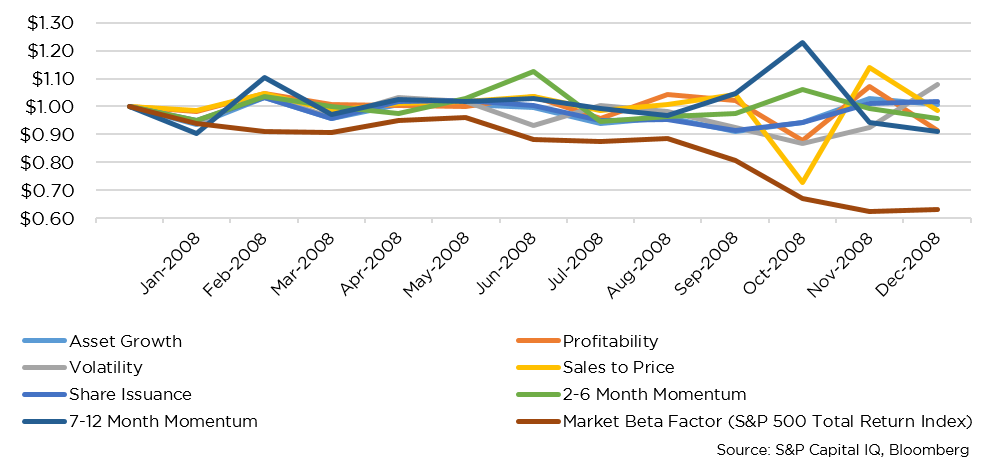

The chart below shows returns to those same factor exposures during the Great Financial Crisis of 2008. Notice how any single factor can experience great volatility. In addition to the broad market, sales to price, profitability, and volatility factors got hammered in late 2008. But momentum factors helped balance out the negativity. This is opposite to the crisis recovery period, where momentum faltered, leaving factor investors dependent on complementary factors (i.e. Volatility, Sales To Price, Profitability) to stay above water.

Financial Crisis: 2008 Value of $1 Invested in Individual Factors

We’ve found the best approach is to optimize portfolio risk exposure by allocating to multiple factors[ii] at the same time. These factors have positive expected returns over the long term, low correlation with the broad stock market, and lower correlation with one another.

Conventional index ownership provides exposure to the single factor of broad economic risk and offers investors a very attractive value proposition over the long term. But a pure indexing approach misses out on a valuable extra source of uncorrelated returns. This multifactor approach adds strategic diversification and provides investors with a potential buffer against the broad economic shocks that prompt so much hand-wringing, emotional portfolio decision-making, and catalogues of scary scenarios in letters to investors.

[i] These hypothetical portfolios went long the top 20% (quintile) ranked stocks of that factor, and went short an offsetting bottom quintile of stocks representing the bottom quintile ranking of all stocks for that same factor. The universe here is US stocks with a market capitalization above $100 million and is rebalanced quarterly. The neutralizing effect of going long-short removes the market factor from the equation, so the portfolio is not affected solely by the market moving up or down. Instead it is moved by changes to valuations determined by factor exposures.

[ii] How you best invest in multiple factors is another discussion. Counterpoint works to optimize portfolio risk exposure by allocating to multiple factors simultaneously. And this is a key distinction versus single-factor approaches. Multifactor models consider stocks that have multiple good or bad things going for them in scoring them, avoiding redundancy. For example, because momentum and value factors are often negatively correlated, a stock that ranks very highly in the momentum characteristic might rank poorly as a value stock. If you owned two funds to capture that exposure, the momentum fund would be long the name while the value fund would be short the same name. You would be paying two management fees for two opposing positions. Multifactor models take this into account and go long (and short) stocks that score well (or poorly) on multiple characteristics. This says nothing of the fact that most single-factor products don’t include the juiciest reason to invest in factor strategies, the short side.